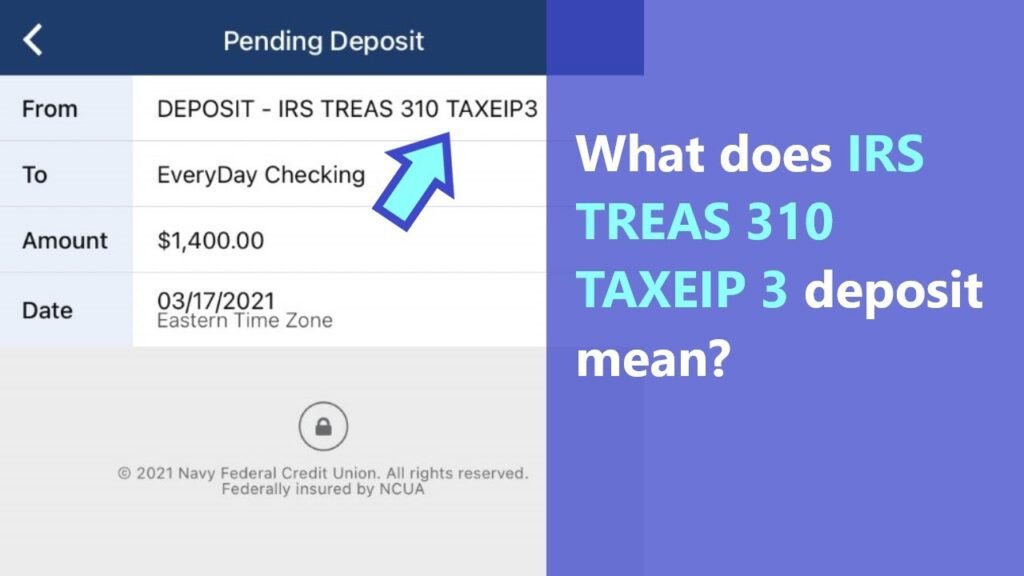

IRS TREAS 310 Tax Ref

Seeing an unfamiliar deposit labeled IRS TREAS 310 TAX REF on your bank statement can immediately cause confusion, especially if you were not expecting a tax refund. Many taxpayers wonder if the payment is legal, related to a recent tax file, or the consequence of an IRS adjustment that they were never alerted about. The IRS often issues refunds after recalculations, math-error corrections, delayed processing, or the release of previously held funds—sometimes depositing the money before sending any explanation. Because the code gives little explanation, taxpayers frequently seek clarification on the source and purpose of the payment.

Why IRS TREAS 310 TAX REF Creates So Much Confusion

The confusion exists for several reasons:

The IRS frequently releases refunds or changes without sending any previous notice.

Bank statements display technical Treasury codes rather than clear descriptions

Payments may refer to past tax years or delayed repairs.

Refunds are sometimes issued in partial amounts

IRS payment timing frequently deviates from what taxpayers expect.

In 2026, these challenges persist as the IRS modernises its systems, clears backlogs, completes older reviews, and processes millions of modified returns from previous years. This detailed guide explains exactly what IRS TREAS 310 TAX REF means, why you may have received the payment, how the IRS processes these deposits, and what steps you should take next.

This page gives complete, expert-level clarity, covering every potential cause for the deposit, the full meaning of the code, bank routing data, year-by-year explanations from 2021 to 2026, identity verification delays, refund offsets, ACH routing identities, and more.

What Is IRS TREAS 310 Tax Ref?

IRS TREAS 310 TAX REF is a legitimate federal payment label issued by the Internal Revenue Service and routed through the United States Treasury. The code identifies electronic payments associated with:

- A federal tax refund

- A tax return correction

- An amended return adjustment

- An overpayment refund

- A credit recalculation

Each part of the label has a specific meaning:

- IRS — Indicates the Internal Revenue Service

- TREAS — Shows the payment is issued by the U.S. Department of the Treasury

- 310 — A Treasury classification code used for ACH deposits

- TAX REF — Confirms the deposit is tied to a tax refund or adjustment

This code does not apply to stimulus funds, Social Security benefits, unemployment compensation, or other state-issued payments. It is specific to federal tax activity handled by the IRS.

Banks may present the same payment in multiple formats, including:

- IRS TREAS 310 TAX REF

- TAX REF IRS TREAS 310

- IRS 310 TREAS TAX REF

- Deposit IRS TREAS 310 TAX REF

- ACH IRS TREAS 310

While the wording varies, the meaning is identical:

You received money from the IRS.

It helps to understand how IRS payments move through banking networks. IRS refunds are transmitted using the Automated Clearing House (ACH) network. Treasury systems create the “310” code automatically. Banks get the data and add extra descriptors based on their internal formatting guidelines. This explains why your bank statement may differ from someone else’s. However, the basic meaning remains unchanged.

What IRS TREAS 310 Tax Ref Means on Your Bank Statement

When this code appears on your bank statement, it indicates your refund or adjustment was processed and released electronically. But this raises new questions for many taxpayers: What refund? From which year? Why now?

Here is the deeper explanation.

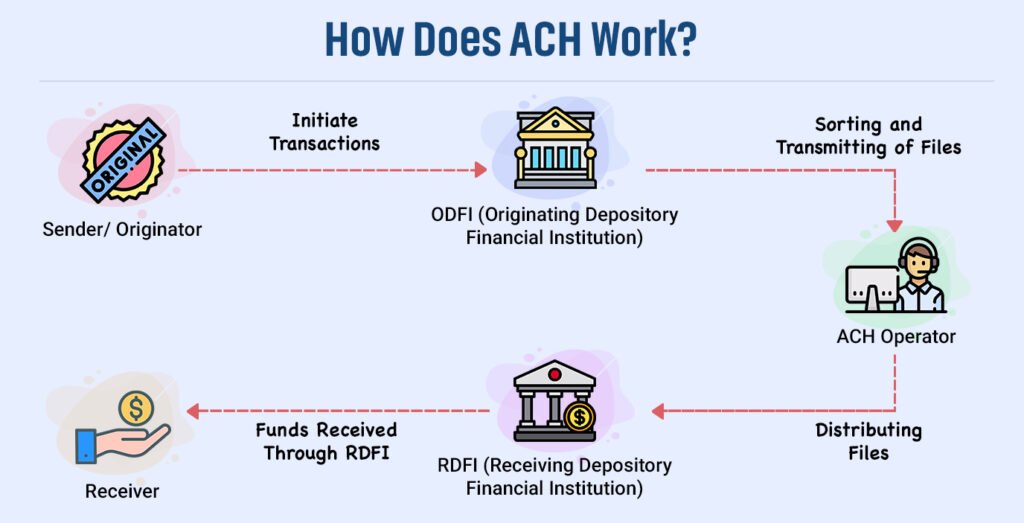

1. The IRS Uses ACH as the Standard Method of Issuing Refunds

The IRS sends most refunds through the Automated Clearing House (ACH) system, which allows funds to be transferred directly into a taxpayer’s bank account. ACH deposits are preferred because they are speedier than paper checks, have a lower risk of fraud, and reduce mail processing delays.

Since the majority of taxpayers now select direct deposit when filing their returns, the code IRS TREAS 310 has become the most common identifier for IRS-issued refunds or adjustments. This promotes consistency in processing and helps banks to appropriately categorize deposits.

2. The Deposit May Relate to a Return Filed Weeks or Months Ago

A refund coded as IRS TREAS 310 TAX REF may not always correspond to your most recent filing. IRS processing times vary, and even minor delays—such as additional identity checks, mismatched employer wage reports, EITC/CTC reviews, or routine error corrections—can push a refund far beyond the typical timeline.

As a result, taxpayers frequently receive unexpected deposits long after they filed. These delays do not always trigger immediate notifications, but the resulting deposit is still tied to a valid IRS action.

3. You May Not Always Receive a Notice Before the Money Arrives

IRS notices like CP12, CP21A, CP24, or CP05 often explain why a refund was corrected or issued. However, these letters frequently arrive after the refund has already reached your bank account.

In many cases, the IRS prioritizes releasing the corrected amount to avoid further delays, while the explanatory notice is still being printed and mailed. This means that taxpayers notice the deposit first and then receive the clarification days or even weeks later. This timing is normal and does not indicate a problem with your refund.

4. The Payment May Relate to an Older Year

An IRS TREAS 310 deposit is not always tied to the current tax year. The IRS routinely reviews past filings, employer corrections, amended returns (Form 1040-X), or previous refund adjustments. When the IRS discovers an overpayment, recalculation, or processing change from a prior year, it may issue a refund automatically—even if the original filing happened one, two, or several years earlier. Taxpayers frequently receive these deposits unexpectedly, particularly when updated returns or audits require a prolonged period to complete.

5. Banks simplify long Treasury descriptions

Some banks truncate descriptions, leaving the meaning unclear. Your bank sees only the ACH routing instruction—not the details behind the payment.

In all cases, IRS TREAS 310 TAX REF means the payment is:

- Legitimate

- Federal

- Tax-related

- Originating from the U.S. Treasury

Is IRS TREAS 310 Tax Ref Federal or State?

This is one of the most asked questions, and the answer is absolute:

IRS TREAS 310 TAX REF is a federal payment.

It cannot come from:

- State tax agencies

- Franchise tax boards

- Local government tax departments

State refunds generally include the name of the state, such as:

- CA Franchise Tax Board Refund

- NY State Tax Refund

- IL Revenue Department

If you see IRS and TREAS, it is unquestionably federal.

What to Do After Receiving IRS TREAS 310 Tax Ref

1. Check your IRS account online

Log in to your IRS online account to review your detailed tax transcripts, refund history, and recent IRS adjustments. This allows you to confirm which tax year or adjustment triggered the deposit and whether any more action is required.

2. Match the amount

Compare the deposit amount with your originally expected refund. A difference may indicate an IRS adjustment, credit recalculation, or offset. Matching the exact figures guarantees that the payment is consistent with your return or amended filing.

3. Review IRS notices

Watch for any mail from the IRS, as notices explaining corrections—such as CP12, CP21A, or CP24—may arrive before or after the refund. These letters offer an official explanation for any tax modifications or refund adjustments.

4. Do not return the money unless IRS tells you

Deposits issued through IRS TREAS 310 TAX REF are typically legitimate. Do not send back funds unless the IRS specifically instructs you in writing. Refund recapture is extremely unusual and is often triggered only by unambiguous IRS contact.

IRS TREAS 310 Tax Ref PPD, ACH & 9111036170 Explained

PPD

Prearranged Payment and Deposit (PPD) is a standardized banking code used for direct deposits from trusted institutions. When associated with IRS TREAS 310, it signals a government-authorized transfer processed through secure federal payment channels.

ACH

ACH, or Automated Clearing House, is the nationwide electronic banking network the IRS uses to distribute refunds and tax adjustments. It assures that monies are routed quickly, securely, and automatically into a taxpayer’s bank account, eliminating the need for physical checks.

PPD ID: 9111036170

This numeric identifier is a Treasury-specific routing code that confirms the ACH deposit originated from an official U.S. government source. Banks use this ID to authenticate the transaction and ensure it is a legitimate IRS-issued payment.

Treasury Offset Program (TOP) & Why Your IRS TREAS 310 Tax Ref May Be Reduced

If your IRS TREAS 310 TAX REF deposit is smaller than expected, the most common reason is the Treasury Offset Program (TOP). This federal system automatically uses part of your refund to pay overdue debts such as past-due child support, defaulted student loans, state taxes, unemployment overpayments, or other federal agency balances.

TOP offsets happen before your refund reaches your bank, which is why the deposit may appear reduced even though your tax return was correct. Notices explaining the offset frequently arrive days or weeks later, so many taxpayers only notice the reduction when they check their bank account.

IRS Notices That Lead to IRS TREAS 310 Tax Ref Deposits

Understanding CP12, CP21A, CP24, CP05, 4883C, 5071C, and Other IRS Letters

Many IRS TREAS 310 TAX REF deposits are triggered by IRS-issued notices that explain why your return was corrected, reviewed, delayed, or adjusted. However, these letters often arrive after the deposit hits your bank account, creating confusion for taxpayers who were never notified beforehand.

The most typical IRS letters for unexpected or corrected refunds are shown below, along with what they indicate and why they require a Treasury 310 deposit.

1. CP12 – Math Error Correction Notice

The CP12 notice is issued when the IRS identifies a mistake on your return involving calculations, income entries, dependents, or refundable credits. If the correction results in a larger refund, the IRS releases the adjusted amount under IRS TREAS 310 Tax Ref. CP12 notices typically arrive days after the refund is made, making the payment appear unexpected or unexplained.

2. CP21A – Refund Adjustment Notice

A CP21A notice indicates the IRS made an adjustment to your previously filed return, often due to updated employer reports, corrected withholding, or credit recalculations. When this modification raises your return, the additional cash is delivered electronically via the 310 code. CP21A adjustments are common for Earned Income Credit, Child Tax Credit, and amended return corrections.

3. CP24 – Overpayment Applied to Other Taxes

This notice is provided when you overpaid a tax year and the IRS uses a portion of the refund to another outstanding tax obligation. If your remaining balance results in a refund, it will be deposited via IRS TREAS 310 Tax Ref. CP24 letters explain how the IRS split or redirected the refund, which is why the deposit may be smaller than expected.

4. CP05 – Refund Under Review

A CP05 notice indicates that the IRS is reviewing your income, credits, or withholding to ensure accuracy. Your refund is temporarily held until the review is completed. When the IRS finishes its checks and approves the refund, the payment is released as IRS TREAS 310 Tax Ref, often with no additional advance notice.

5. 4883C – Identity Verification Required

If the IRS suspects identity theft or inconsistencies on your return, you may receive a 4883C letter asking you to verify your identity. Your reimbursement is on hold until verification is complete. Once cleared, the IRS releases the refund quickly, and you may see a sudden “310” deposit appear before receiving any follow-up communication.

6. 5071C – Online ID Verification Request

Similar to 4883C, the 5071C notice directs taxpayers to verify their identity online. After satisfactory verification, the reimbursement is processed and provided. Because verification clears large batches of returns at once, many taxpayers see their refund appear unexpectedly as an IRS TREAS 310 deposit.

7. Letters Delayed but Refund Released First

Mail delays are common. Even when the IRS generates a notice explaining an adjustment or correction, the letter may arrive 7–30 days after the refund. This delay often leads taxpayers to believe that the deposit is random.

Seeing money appear unexpectedly in your bank account, especially if it is designated IRS TREAS 310 TAX REF, might be confusing or even suspicious. Many taxpayers instantly inquire:

8. Will Future Returns Also Require Verification?

Possibly. Once your SSN has been flagged for identity protection, the IRS may apply additional safeguards on future returns. You may be required to:

- Verify your identity again

- Use a special PIN (IP PIN)

- Confirm your filing method or address

IRS Identity Verification & How It Impacts Your IRS TREAS 310 Tax Ref Deposit

Identity verification has become one of the major causes of IRS refund delays in 2026. When a tax return is flagged for possible identity theft, mismatched wage data, or unusual filing activity, the IRS places a temporary hold on the refund until the taxpayer completes verification through a 4883C or 5071C letter.

Once verification is completed, the IRS typically releases the refund quickly—often resulting in a sudden IRS TREAS 310 Tax Ref deposit with little or no prior notice. Many taxpayers notice the money appear before receiving a revised transcript or confirmation letter.

If your refund is delayed and you’ve recently verified your identity, a surprise deposit is usually a sign that your return was cleared and moved back into processing.

How Banks Process IRS TREAS 310 ACH Deposits

Understanding ACH cycles, bank posting rules, early deposits, delays, and why refunds appear on different days.

Even after the IRS issues your refund, the deposit may not immediately reach your bank. All IRS refunds coded as IRS TREAS 310 Tax Ref move through the Automated Clearing House (ACH) system—a nationwide network used by banks, credit unions, and federal agencies to process electronic transfers.

Because each financial institution posts ACH deposits differently, two taxpayers may receive their refunds on completely different days even if the IRS released them at the same time.

Understanding how banks manage these payments explains why a return may arrive early, late, or unexpectedly.

1. How ACH Settlement Works for IRS Refunds

When the IRS releases a refund, the payment is sent to the Federal Reserve for batch settlement rather than individual real-time disbursement. The Federal Reserve then transmits the deposit to your bank through ACH files that banks receive:

- Early morning (most common)

- Mid-day (occasionally)

- Evening batches (smaller banks)

Banks do not receive IRS refunds continuously—only in scheduled ACH windows. This is why refund deposits often appear:

- Very early in the morning

- At the same time every year

- In specific bank posting cycles

If your bank misses the morning window, the deposit may not appear until the next ACH posting cycle.

2. Why Some Banks Release IRS Refunds Early

Banks like Chime, Varo, Cash App, Netspend, Capital One, and certain credit unions advertise “early deposit.”

They do this by:

- Accepting ACH files as soon as they receive them

- Posting pending deposits immediately

- Not waiting for the Federal Reserve settlement confirmation

This means that taxpayers utilizing these institutions frequently receive IRS TREAS 310 deposits 1-2 days early than regular banking customers.

3. Why Some Banks Delay Posting Refunds

Traditional banks, like Chase, Wells Fargo, Bank of America, US Bank, and many regional credit unions, hold deposits until the official settlement date. Their delays happen because:

- They follow conservative clearing policies

- They verify the origin of federal deposits

- They batch-post deposits overnight only

- Fraud prevention algorithms delay high-dollar refunds

This is why IRS TREAS 310 deposits sometimes do not post:

- On weekends

- On federal holidays

- After 5 PM local time

- During system maintenance windows

The IRS may disburse a refund on a Friday, but it will not arrive in your bank account until Monday or Tuesday.

4. Banking Factors That Affect Refund Timing

Several internal bank processes determine exactly when your refund posts:

Cutoff Times

If your bank’s daily cutoff is 3 p.m. and the IRS settlement occurs at 4 p.m., your deposit will not appear until the following morning.

Weekend & Holiday Rules

Federal payments cannot settle on holidays or weekends.

ACH deposits scheduled on these days move to the next business day.

Fraud & Identity Checks

Large refunds may trigger bank-level holds or temporary delays to prevent unauthorized activity.

Time Zone Differences

Banks on the West Coast frequently post refunds later than banks on the East Coast due to ACH scheduling variations.

5. Why Deposits Arrive at Weird Hours (Midnight, 2 AM, 5 AM)

Most IRS TREAS 310 deposits post during:

- 12 AM – 3 AM (ACH first batch)

- 4 AM – 6 AM (final batch)

This is because banks update their systems overnight when demand on their networks is low.

If you check your bank app early in the morning, you may notice the deposit arrive unexpectedly during this time.

6. When the IRS Shows “Refund Issued” But the Bank Has No Deposit

It is normal for the IRS transcript to display Code 846 – Refund Issued, but no money appears in your bank account.

This happens because:

- ACH settlement is not instant

- Banks have internal posting delays

- Some banks do not post deposits until 9 AM–10 AM

- Weekends push deposits to Monday

- Holidays add additional delays

Typical timeline after Code 846:

- 2-5 business days for the deposit to fully process.

7. When the Bank Shows the Deposit Before the IRS Transcript Updates

This also happens frequently. Reasons include:

- Banks receive Treasury ACH files earlier

- IRS transcript systems refresh once daily

- Transcript lag can be 24–72 hours

- Weekend/holiday cycles delay transcript updates

Many taxpayers see their IRS TREAS 310 Tax Ref before their transcript reflects it.

8. Split Deposits and Partial Refunds

Sometimes you may see:

- Two separate TREAS 310 deposits

- One large deposit followed by a small “adjustment”

- A deposit that doesn’t match your expected refund

Bank processing does NOT split refunds.

If the amounts differ, it almost always relates to:

- Treasury Offset Program (TOP)

- IRS credit recalculations

- Identity verification timing

- Multiple-year refunds processed together

Your transcript will indicate which one applies.

9. Why Your Friend Received Their Refund Before You

Even with identical filing dates and refund amounts, differences occur due to:

- Bank posting cycles

- Batch settlement variations

- Deposit holds

- Identity or wage verification delays

- Weekends or holidays

- Differences between early-deposit vs. traditional banks

The IRS does not prioritize refunds solely based on filing order; bank activity also plays an important role.

IRS Interest Payments Explained (Why You May See Extra Money With Your IRS TREAS 310 Tax Ref)

Some taxpayers receive more money than expected in their bank account, showing descriptions like IRS TREAS 310 INT REF or TAX REF + Interest. This extra amount is an interest payment issued by the IRS when your refund is delayed beyond the legally authorized term. If the IRS takes longer than 45 days to process your return—due to backlogs, identity verification, amended returns, or credit mismatches—you earn interest automatically.

Interest payments can appear months or even years later, sometimes with no prior notice. They are fully legitimate and will also appear on your IRS transcript with codes such as 776 (Interest Credit) and 846 (Refund Issued). While the payment may appear unexpected, it only compensates for the delay in issuing your return.

Amended Returns (1040-X) & Why They Trigger Unexpected IRS TREAS 310 Tax Ref Deposits

Many taxpayers are unaware that the IRS may provide extra refunds months—or even years—after an updated return is filed. Amended returns take significantly longer to process than standard filings, often resulting in sudden, unexplained IRS TREAS 310 Tax Ref deposits long after the taxpayer has forgotten about the correction.

If you filed Form 1040-X or the IRS made its own adjustment to a prior-year return, this section explains why you may receive a deposit unexpectedly.

1. Why Amended Returns Take 16–20+ Weeks to Process

Amended returns require manual review, which means that an IRS agent must compare your original return to the revised form. Processing times often stretch to:

- 16–20 weeks during normal periods

- 20–30+ weeks during high-volume seasons

- Even longer during years with staffing shortages or backlogs

Because modified returns move slowly, taxpayers frequently forget they filed one by the time the refund arrives.

2. Common Reasons Amended Returns Lead to Additional Refunds

You may receive a TREAS 310 deposit due to:

Revised income or withholding

Correcting missing W-2s, 1099s, or incorrect employer data can increase your refund.

Credit adjustments

Changes to the Child Tax Credit, Earned Income Credit, American Opportunity Credit, and Saver’s Credit frequently affect the return amount.

Filing status corrections

Switching from single to head of household, or updating dependents, can result in a larger refund.

Overpayment discovered after IRS review

Even when no 1040-X is submitted, the IRS occasionally discovers an error that benefits the taxpayer.

Late employer corrections

If your employer files a corrected W-2 (W-2C), the IRS may adjust your tax automatically.

In all of these circumstances, the revised alteration results in a recalculated refund.

3. Why Amended Return Refunds Appear Without Warning

Although modified returns should generate a written notice, the IRS frequently issues refunds before delivering mailed explanations.

This happens because:

- IRS systems finalize payments faster than the mailroom prints notices

- Transcript updates lag behind refund release

- High backlog years prioritize payment before documentation

- Many notices go to old mailing addresses

- Mail delivery takes 5–20+ days

As a result, the IRS TREAS 310 deposit may appear before you receive any letter, explanation, or transcript update.

4. Transcript Codes That Identify Amended Return Refunds

If your deposit is tied to a 1040-X or IRS correction, you’ll usually see:

- Code 290 — Additional tax assessed (sometimes $0)

- Code 291 — Reversal of tax increase

- Code 766 — Credit to your account

- Code 767 — Miscellaneous credit

- Code 846 — Refund issued

In amended-return cases, the 846 refund number frequently emerges months after the original transcript activity.

5. Why Amended Return Refunds May Be Partial or Split

Your amended refund may not match the amount you calculated on your 1040-X. Common reasons include:

Treasury Offset Program deductions

Child support, college loans, and state debts limit your refund.

IRS recalculations beyond your amendment

An IRS agent may find additional corrections—both positive and negative.

Multiple tax years adjusted at once

It is possible to receive a combined refund for multiple years.

Credit adjustments applied after approval

EITC or CTC changes may alter the final amount.

This explains why modified refunds appear to come in unexpected amounts.

6. How Long After Filing 1040-X You Should Expect a Refund

General timelines:

- 8–12 weeks: IRS acknowledges receipt

- 12–20 weeks: IRS completes manual review

- 16–30+ weeks: Refund issued for most taxpayers

- 30–52 weeks: Cases involving identity verification, missing documents, or wage mismatches

If your updated return includes credits or dependent adjustments, processing time will be longer.

7. When You Should Call the IRS About an Amended Refund

You should contact the IRS only if:

- More than 30 weeks have passed

- Transcript shows no movement after receipt

- Refund amount differs drastically from what you expected

- Freeze codes (810 or 570) remain unresolved

- You never filed an amendment but still received an “adjustment refund”

Unexpected refunds should always be checked, but IRS errors in your favor are exceedingly uncommon.

Scam & Fraud Prevention: How to Confirm Your IRS TREAS 310 Deposit Is Real

Protecting yourself from tax scams, fake refunds, and fraudulent communications in 2026.

Because IRS deposits often appear without warning, many taxpayers worry whether an unexpected IRS TREAS 310 TAX REF deposit is legitimate or part of a scam. Fortunately, genuine IRS deposits adhere to tight standards, formats, and verification procedures. Fraudulent transfers, on the other hand, show clear warning indicators.

This section explains how to confirm that your deposit is genuine and how to avoid becoming a victim of refund-related scams.

1. The IRS Never Calls, Texts, or Emails About Refund Deposits

If a deposit appears in your bank, the IRS will never:

- Call you asking for personal information

- Text you a link

- Email you instructions

- Ask you to “verify” your bank account

- Demand that you return the refund immediately

Any such communication is a scam.

2. Real IRS Deposits Always Include Specific Banking Codes

Legitimate IRS refunds delivered through ACH will show one of the following:

- IRS TREAS 310 Tax Ref

- IRS TREAS 310 INT Ref

- IRS TREAS 310 MISC (rare)

Additionally, real deposits may include a PPD ID such as 9111036170, confirming the deposit came from the U.S. Treasury.

Scammers cannot replicate these codes through legitimate ACH channels.

3. How to Verify a Refund Is Genuine Using IRS Tools

Check Your IRS Online Account

Your online IRS transcript will show the refund under:

- Code 846 — Refund Issued

- Code 776 — Interest Paid (if applicable)

- If no transcript activity exists, the deposit may be a bank error.

Compare Deposit Amount to Your Refund Status

If the deposit does not match:

- Your expected refund

- A corrected amount

- A known amended return

You should verify through IRS transcripts before taking any action.

4. The IRS Will Never Ask You to Return Money Unexpectedly

One of the most common refund scams involves messages claiming:

“You received a deposit by mistake; send the money back.”

The IRS never instructs taxpayers to return refunds via:

- Gift cards

- Wire transfers

- Mobile payment apps

- Cryptocurrency

- Prepaid debit cards

If the IRS truly needs to recover funds, they will:

- Send a written notice

- Provide an official payment process

- Adjust future refunds-not demand immediate payment

Refund recapture is rare and always done in writing.

5. Beware of Fake Refunds and Bank Transfer Scams

Some scammers deposit fake electronic checks into bank accounts, then pretend it was an IRS overpayment. They ask the victim to:

- Transfer money back

- Buy gift cards

- Send “excess” refund through PayPal or Zelle

When the check later bounces, the victim loses their own money.

Important:

The IRS does not use “checks” for surprise refunds. IRS TREAS 310 deposits only come through ACH.

6. Signs the Deposit Is NOT From the IRS

You should be cautious if:

- The description does not include “IRS TREAS 310”

- The bank lists the source as a personal transfer

- The deposit posts as a check, not an ACH

- Someone contacts you immediately afterward

- You receive a message urging quick repayment

- The deposit appears in a savings account you never use for tax refunds

In these cases, contact your bank before touching the funds.

7. What to Do If You Suspect a Fake or Incorrect Deposit

If something feels wrong:

Step 1: Check your IRS Account Transcript

If the refund is not listed as Code 846, it may not be from the IRS.

Step 2: Contact Your Bank

Ask whether the deposit originated from the U.S. Treasury.

Step 3: Do NOT spend the money until verified

Incorrect deposits can be reversed by your bank.

Step 4: Contact the Treasury Inspector General (TIGTA)

Report refund-related scams at: www.tigta.gov

8. Common IRS-Related Scams to Avoid in 2026

- Fake identity verification emails

- Phishing messages claiming “Account Frozen”

- Texts about refund delays

- Fake CP notices with QR codes

- Messages asking you to “verify refund amount”

Remember:

The IRS does not initiate contact through email, text, or social media.